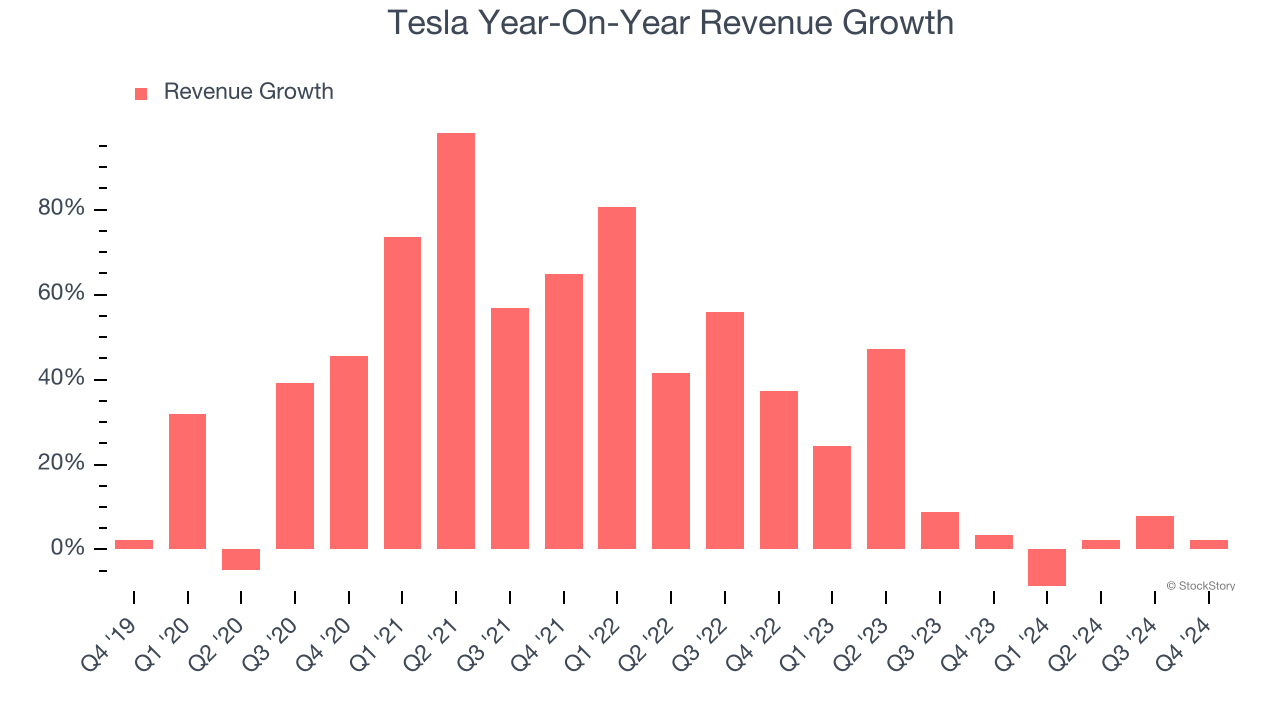

Electric vehicle pioneer Tesla (NASDAQ:TSLA) fell short of the market’s revenue expectations in Q4 CY2024 as sales rose 2.1% year on year to $25.71 billion. Its non-GAAP profit of $0.73 per share was 5.2% below analysts’ consensus estimates.

Is now the time to buy Tesla? Find out by accessing our full research report, it’s free.

Tesla (TSLA) Q4 CY2024 Highlights:

- Aims to launch unsupervised FSD and Robotaxi businesses later this year

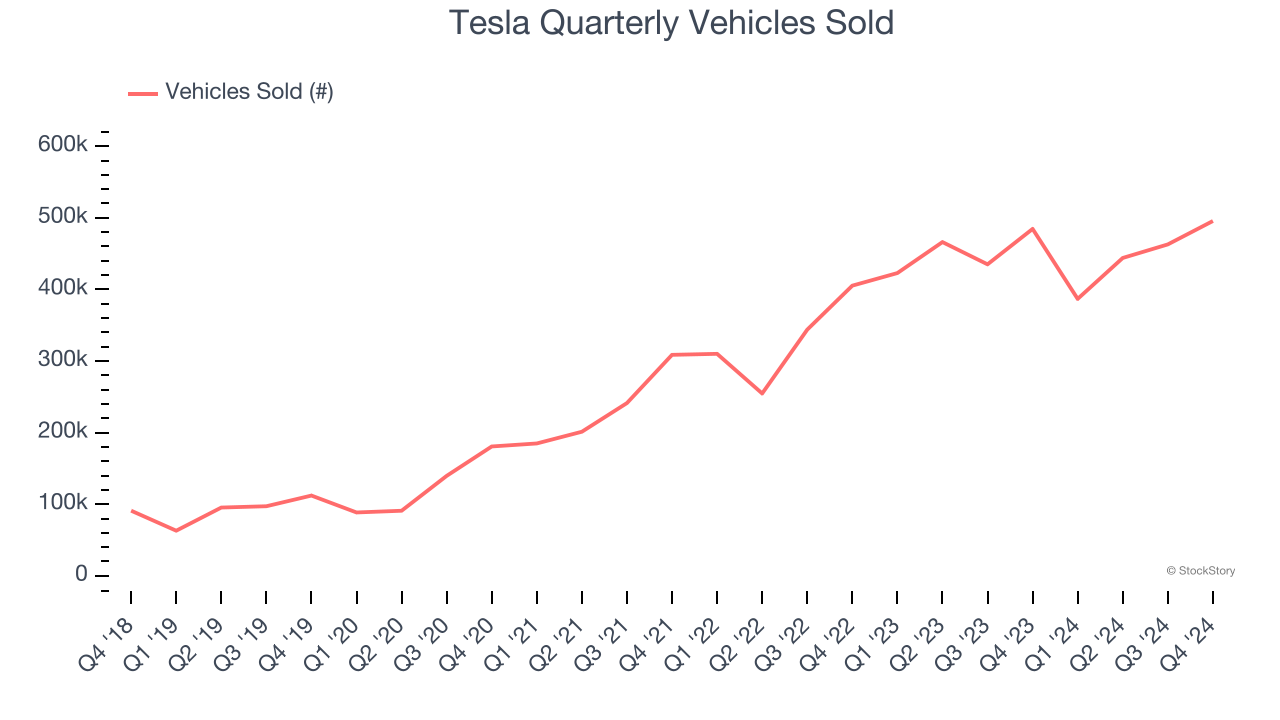

- Vehicles Delivered: 495,570 vs analyst estimates of 503,106 (1.5% miss)

- Revenue: $25.71 billion vs analyst estimates of $27.35 billion (6% miss)

- Operating Profit (GAAP): $1.58 billion vs analyst estimates of $2.7 billion (41.5% miss)

- EPS (non-GAAP): $0.73 vs analyst expectations of $0.77 (5.2% miss)

- Automotive Revenue: $19.8 billion vs analyst estimates of $21.41 billion (7.5% miss)

- Energy Revenue: $3.06 billion vs analyst estimates of $3.13 billion (2.3% miss)

- Services Revenue: $2.85 billion vs analyst estimates of $2.81 billion (1.3% beat)

- Gross Margin: 16.3%, down from 17.6% in the same quarter last year

- Operating Margin: 6.2%, down from 8.2% in the same quarter last year

- Free Cash Flow Margin: 7.9%, in line with the same quarter last year

- Market Capitalization: $1.28 trillion

Key Topics & Areas Of Debate

The vast majority of Tesla’s revenue (78.9%) comes from electric vehicle (EV) sales, making metrics like units delivered and average sale price crucial for our analysis. However, two emerging questions are shifting the conversation beyond just car sales.

Can the Services segment - mainly consisting of low-margin maintenance and repairs today - decouple from vehicle sales with Tesla’s new AI-driven products?

Sparking hope for bulls are new technologies like Full Self-Driving (FSD) and a potential robotaxi fleet. If successfully commercialized, they could not only supercharge top-line growth but also lift Services gross margin from the high-single-digit percentages.

The second question is whether Tesla’s Energy Generation and Storage division could approach the value of its automotive business. While this may seem farfetched since Energy contributed just 10.3% of revenue last year, a case can be made.

GenAI applications could be the catalyst that accelerates this business as they require vast amounts of computational power. Furthermore, as energy disruptions from extreme weather become more frequent, Tesla’s products could emerge as critical infrastructure.

One standout product we’re closely watching in the Energy segment its Megapack, a large-scale battery system that stores and distributes massive amounts of electricity. Each Megapack can power 100 to 150 homes for 24 hours and sells for over $1 million. Megapacks also have higher margins than EVs - in fact, a single Megapack sale generates as much operating profit as around 100 Tesla automobiles.

If Tesla can scale its Energy business and expand its software Services offerings, the growth potential is enormous and could settle the debate once and for all.

Revenue Growth

Tesla shows that fast growth and massive scale can coexist despite the conventional wisdom about the law of large numbers. The company’s revenue base of $24.58 billion five years ago has nearly quadrupled to $97.69 billion in the last year, translating into an incredible 31.8% annualized growth rate.

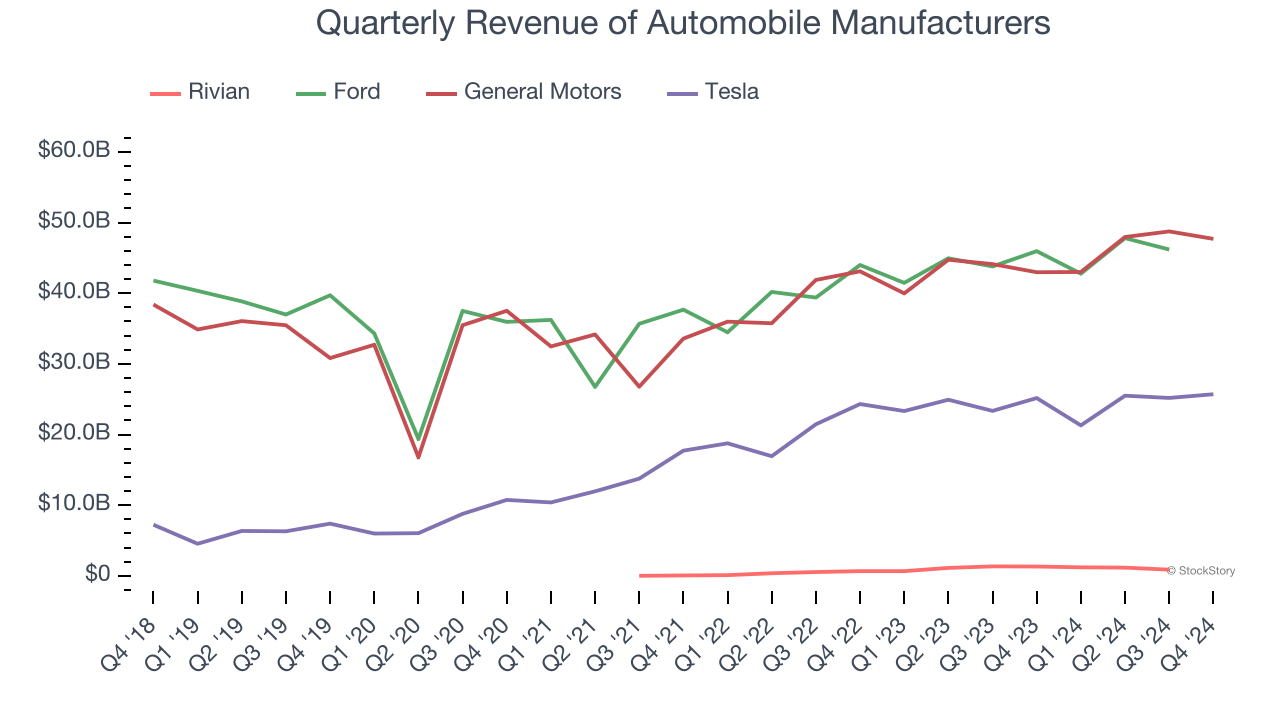

Over the same period, Tesla’s automotive peers Rivian, General Motors, and Ford put up annualized growth rates of 108%, 6.4%, and 3%, respectively. Just note that even though Rivian has the most similar vehicles to Tesla, comparisons aren’t exactly apples-to-apples because it’s growing from a much smaller revenue base and selling its EVs at a loss.

We at StockStory emphasize long-term growth, but for disruptive companies like Tesla, a half-decade historical view may miss emerging trends in autonomous vehicles and energy. Tesla’s annualized revenue growth of 9.5% over the last two years is below its five-year trend, but we still think the results were good and suggest demand was strong.

This quarter, Tesla’s revenue grew by 2.1% year on year to $25.71 billion, falling short of Wall Street’s estimates. Looking ahead, sell-side analysts expect revenue to grow 16.9% over the next 12 months, an improvement versus the last two years. This projection is admirable for a company of its scale and illustrates the market is baking in success for its newer products.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Automotive: Act One

Revenue: The Race For Dominance

Tesla is primarily an automobile manufacturer today and generates 78.9% of its revenue through the sale and leasing of EVs. It historically produced expensive, high-end EVs, but after years of operating losses, has shifted its focus to the mass market with affordable vehicles. The Model 3 and Model Y (released in 2017 and 2019) are the headliners of this story, and we’ll dive into their impacts below.

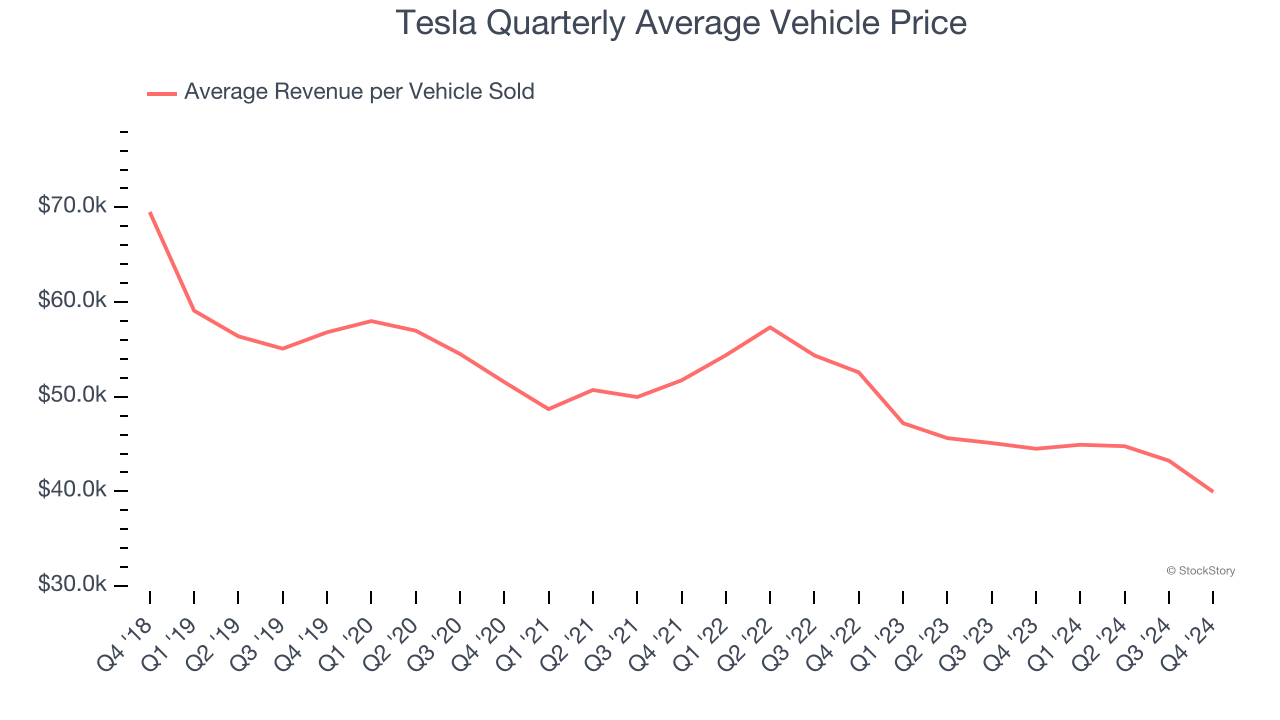

Over the last five years, Tesla’s vehicles sold grew by 37.2% annually to 1.79 million units in the last year. This is meaningfully above the its 29.9% annualized growth rate for Automotive revenue, implying that its average vehicle price fell.

Specifically, Tesla's average revenue per vehicle sold was $43,074 for the trailing 12 months, noticeably lower than the $56,633 price tag in 2019.

These unit and pricing trends uncover three facets of the company’s automotive business:

1) It has achieved its goal of selling more Model 3 and Model Y vehicles, which carry lower price tags than other models, 2) the scaling production of its mass-market models is boosting manufacturing efficiency because it lowers the fixed cost per vehicle sold, and 3) rather than increasing profitability by reaping the cost-saving benefits, Tesla is passing them to customers through price reductions so it can undercut its competitors and capture more market share.

In Q4, Tesla’s vehicles sold shrank by 2.3% year on year to 495,570 units and missed Wall Street’s expectations. Putting this print side-by-side with its 8.2% Automotive revenue decline suggests an average vehicle price of $39,950, down from $44,505 in the same quarter last year.

Unit Economics: The Impact Of Price Cuts

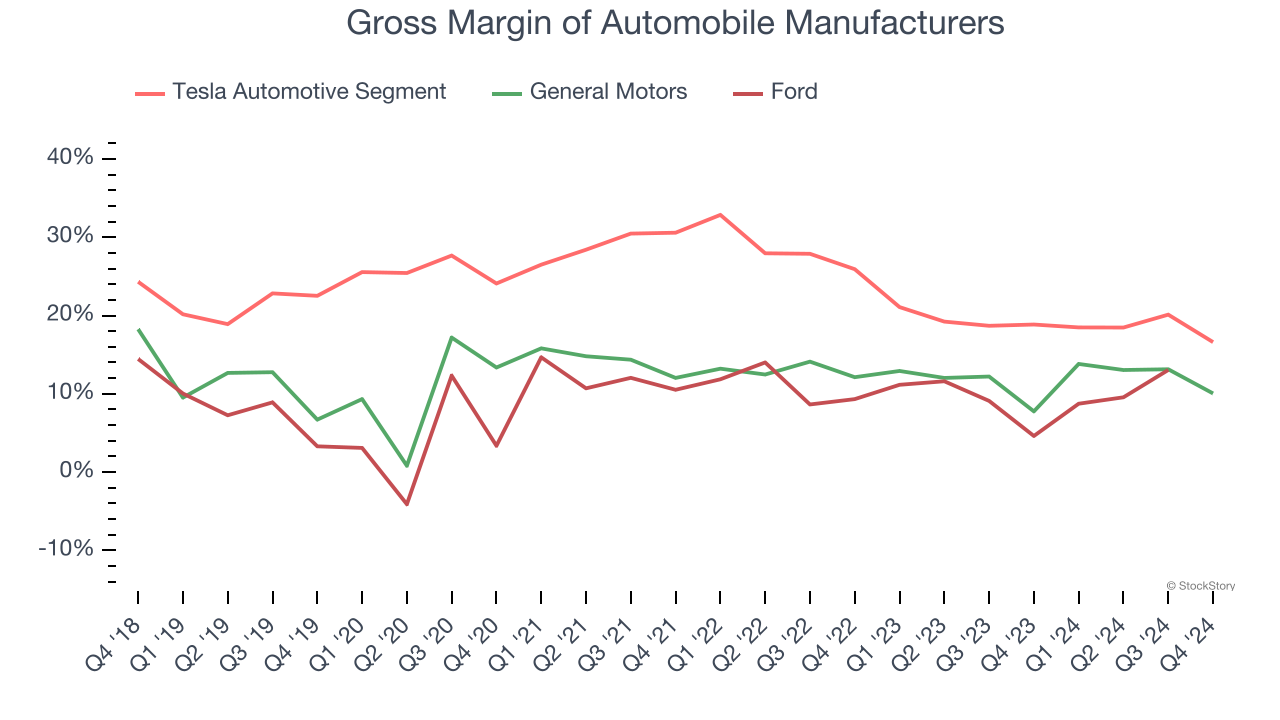

There’s no denying automobile manufacturing is a tough business. Few upstarts succeed because incumbents like General Motors and Ford can afford to break even on the initial sale of vehicles and instead make money on parts and servicing, which come many years down the line. This is why new entrants such as Rivian have negative gross margins - they must price competitively, and their fleets are too young to generate substantial aftermarket revenues.

Tesla does not disclose the operating profitability of its segments, but we can analyze the gross margins of its various divisions to see how it stacks up. For Automotive, this metric reflects how much revenue is left after paying for the raw materials, components, and direct labor costs that go into manufacturing and producing its vehicles.

Thankfully for investors, Tesla has crossed the chasm as its Automotive segment boasted an average gross margin of 23.4% over the last five years. While it may be low in absolute terms, Tesla’s margin was best in class for the industry and illustrates its superior pricing power and procurement capabilities. Its breathing room also explains why the company can squeeze its competitors by slashing prices.

Looking under the hood, Automotive’s annual gross margin fell from 21.2% five years ago to 18.4% in the last year. This is a direct result of its price cuts and shows the company is sacrificing higher profits today to increase its installed base and potentially secure longer-term recurring revenue streams. Still, the trend worsened this quarter as its gross margin was 16.6%.

Key Takeaways from Tesla’s Q4 Results

We struggled to find many positives in these results as its revenue and operating income fell short of Wall Street’s estimates. This performance was driven by underperformance in its Automotive and Energy segments, as Services (which includes full self-driving) actually beat analysts' revenue expectations. However, Services is Tesla's lowest margin business line - it had an extremely bad gross margin of 5.8% for the trailing 12 months, and it fell to 4.2% this quarter.

Overall, this was a weaker quarter, but the stock traded up 3.9% to $403.01 immediately following the results because the company promised investors it would launch its unsupervised full self-driving (FSD) and Robotaxi businesses later this year.

Big picture, is Tesla a buy here and now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.