Over the past six months, Health Catalyst has been a great trade, beating the S&P 500 by 7.9%. Its stock price has climbed to $7.09, representing a healthy 17.2% increase. This was partly thanks to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is there a buying opportunity in Health Catalyst, or does it present a risk to your portfolio? Get the full stock story straight from our expert analysts, it’s free.We’re happy investors have made money, but we don't have much confidence in Health Catalyst. Here are three reasons why HCAT doesn't excite us and a stock we'd rather own.

Why Is Health Catalyst Not Exciting?

Founded by healthcare professionals Tom Burton and Steve Barlow in 2008, Health Catalyst (NASDAQ:HCAT) provides data and analytics technology to healthcare organizations, enabling them to improve care and lower costs.

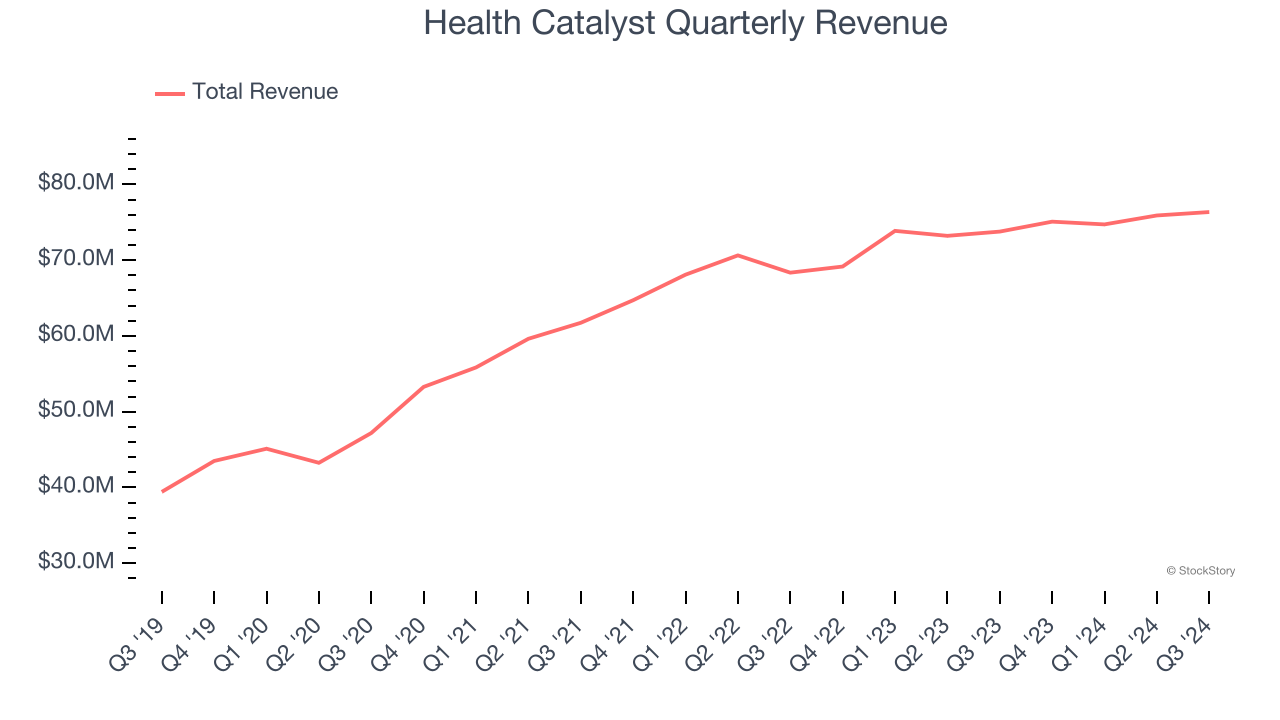

1. Long-Term Revenue Growth Disappoints

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last three years, Health Catalyst grew its sales at a sluggish 9.4% compounded annual growth rate. This was below our standard for the software sector.

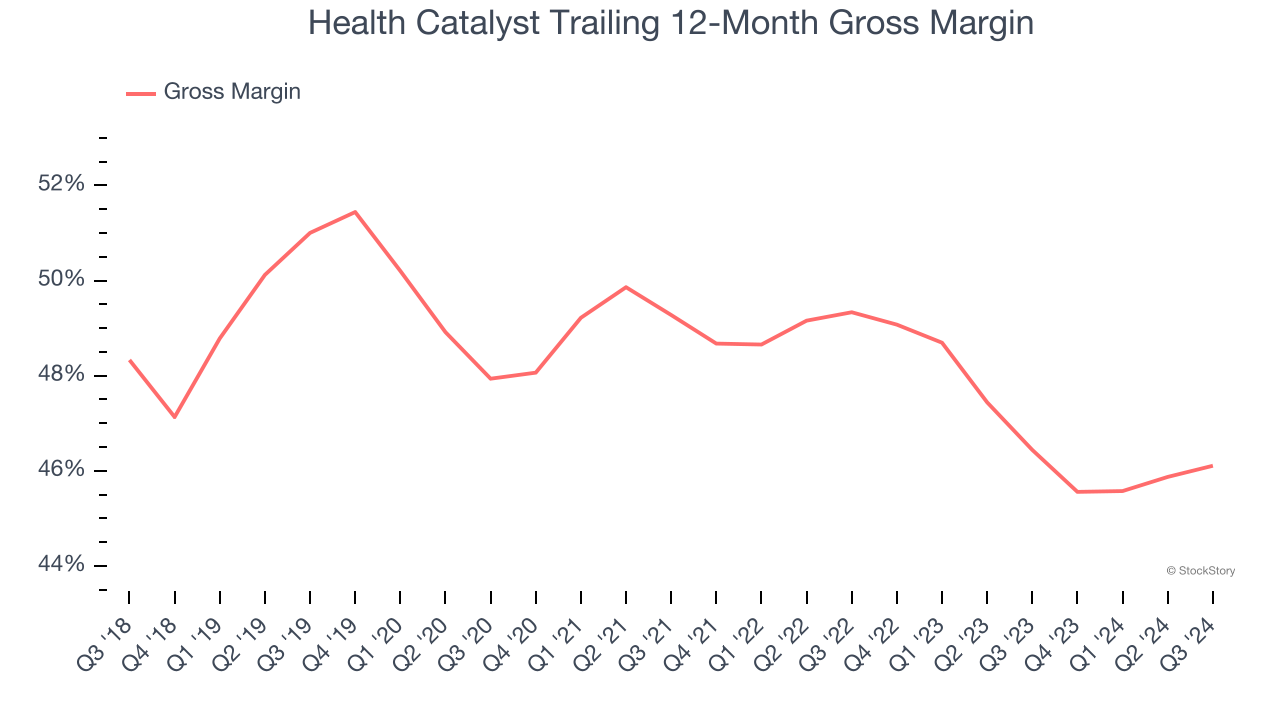

2. Low Gross Margin Reveals Weak Structural Profitability

For software companies like Health Catalyst, gross profit tells us how much money remains after paying for the base cost of products and services (typically servers, licenses, and certain personnel). These costs are usually low as a percentage of revenue, explaining why software is more lucrative than other sectors.

Health Catalyst’s gross margin is substantially worse than most software businesses, signaling it has relatively high infrastructure costs compared to asset-lite businesses like ServiceNow. As you can see below, it averaged a 46.1% gross margin over the last year. Said differently, Health Catalyst had to pay a chunky $53.89 to its service providers for every $100 in revenue.

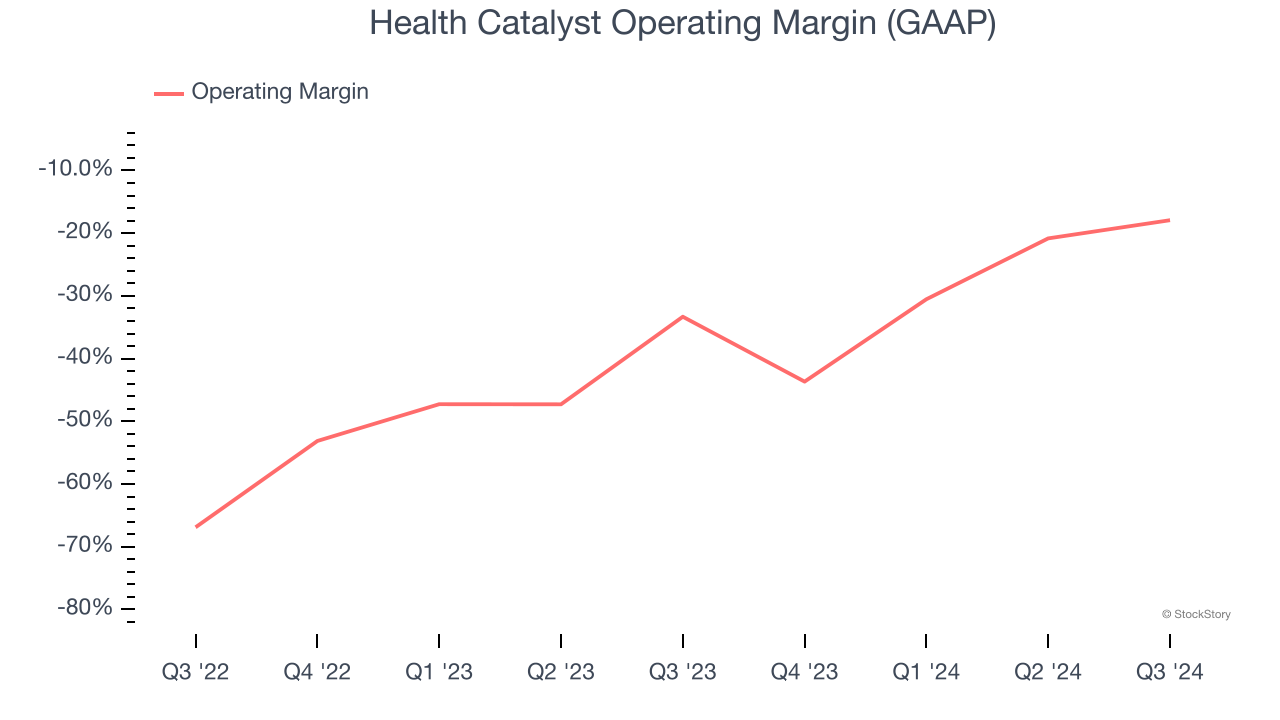

3. Operating Losses Sound the Alarms

While many software businesses point investors to their adjusted profits, which exclude stock-based compensation (SBC), we prefer GAAP operating margin because SBC is a legitimate expense used to attract and retain talent. This metric shows how much revenue remains after accounting for all core expenses – everything from the cost of goods sold to sales and R&D.

Health Catalyst’s expensive cost structure has contributed to an average operating margin of negative 28.2% over the last year. Unprofitable software companies require extra attention because they spend heaps of money to capture market share. As seen in its historically underwhelming revenue performance, this strategy hasn’t worked so far, and it’s unclear what would happen if Health Catalyst reeled back its investments. Wall Street seems to be optimistic about its growth, but we have some doubts.

Final Judgment

Health Catalyst isn’t a terrible business, but it isn’t one of our picks. With its shares topping the market in recent months, the stock trades at 1.3× forward price-to-sales (or $7.09 per share). While this valuation is fair, the upside isn’t great compared to the potential downside. We're pretty confident there are more exciting stocks to buy at the moment. We’d recommend looking at Meta, a top digital advertising platform riding the creator economy.

Stocks We Would Buy Instead of Health Catalyst

The Trump trade may have passed, but rates are still dropping and inflation is still cooling. Opportunities are ripe for those ready to act - and we’re here to help you pick them.

Get started by checking out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,691% between September 2019 and September 2024) as well as under-the-radar businesses like United Rentals (+550% five-year return). Find your next big winner with StockStory today for free.