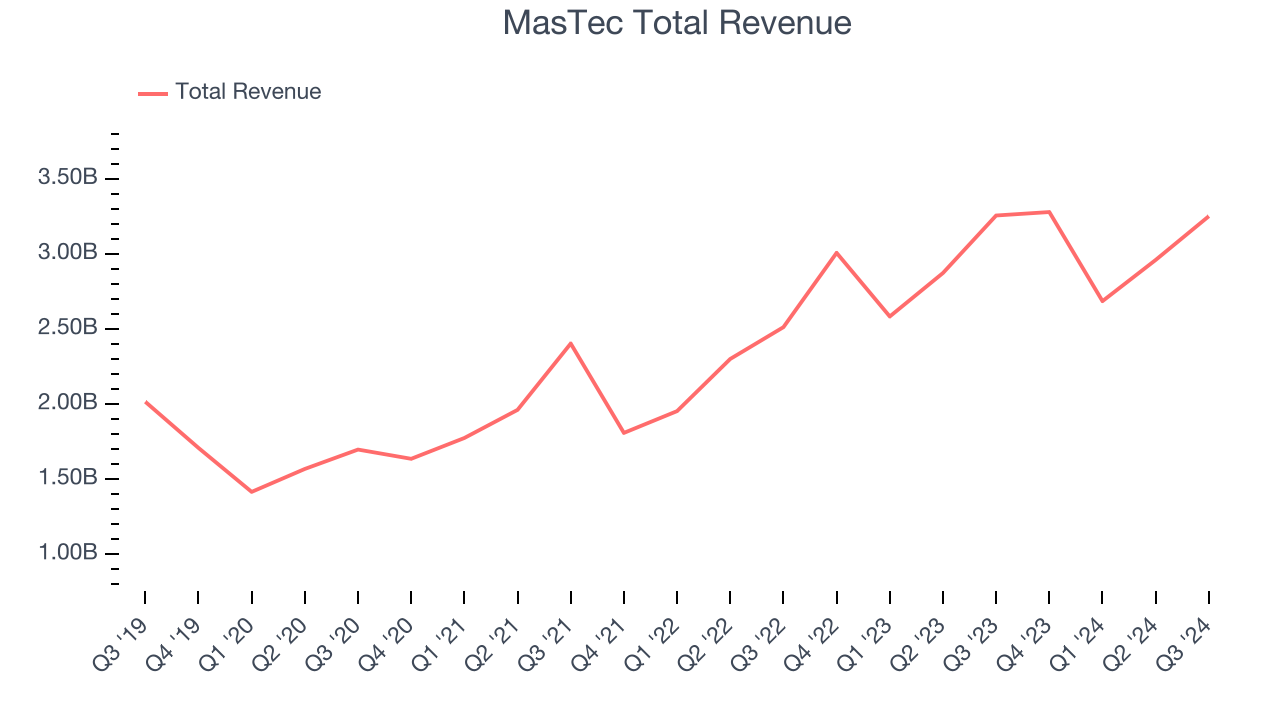

Infrastructure construction company MasTec (NYSE:MTZ) fell short of the market’s revenue expectations in Q3 CY2024, with sales flat year on year at $3.25 billion. On the other hand, the company expects next quarter’s revenue to be around $3.33 billion, close to analysts’ estimates. Its non-GAAP profit of $1.63 per share was 32.3% above analysts’ consensus estimates.

Is now the time to buy MasTec? Find out by accessing our full research report, it’s free.

MasTec (MTZ) Q3 CY2024 Highlights:

- Revenue: $3.25 billion vs analyst estimates of $3.44 billion (5.4% miss)

- Adjusted EPS: $1.63 vs analyst estimates of $1.23 (32.3% beat)

- EBITDA: $305.9 million vs analyst estimates of $293.2 million (4.3% beat)

- Revenue Guidance for Q4 CY2024 is $3.33 billion at the midpoint, roughly in line with what analysts were expecting

- Management raised its full-year Adjusted EPS guidance to $3.75 at the midpoint, a 23.8% increase

- EBITDA guidance for the full year is $990 million at the midpoint, above analyst estimates of $974.5 million

- Gross Margin (GAAP): 14.2%, up from 12.4% in the same quarter last year

- EBITDA Margin: 9.4%, up from 8.3% in the same quarter last year

- Free Cash Flow Margin: 8.5%, similar to the same quarter last year

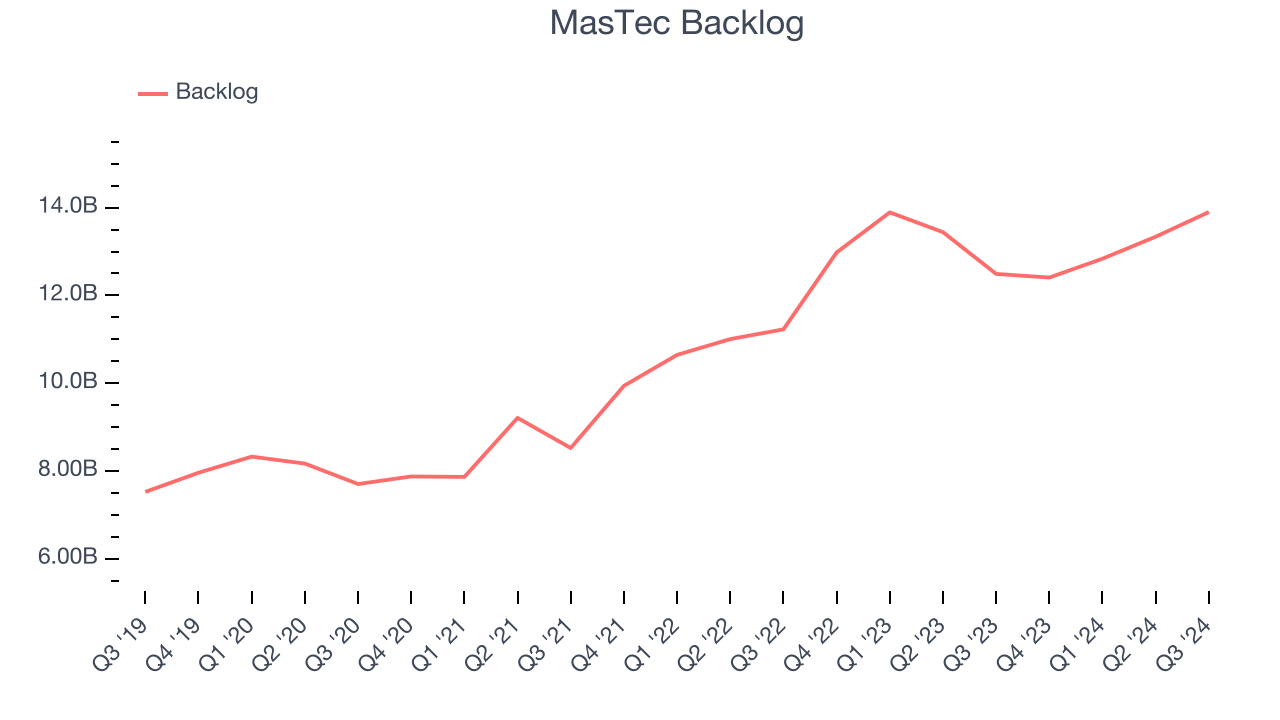

- Backlog: $13.9 billion at quarter end, up 11.3% year on year

- Market Capitalization: $9.35 billion

Jose Mas, MasTec's Chief Executive Officer, commented, "I am pleased with our margin expansion that exceeded our guidance and which drove excellent bottom line performance. Once again, our record backlog and bookings in multiple segments illustrate the strength of our diversified business model and provide good visibility to the work that will drive MasTec's performance in 2025 and beyond. I also want to recognize the hard work and dedication of the men and women of MasTec who continue to deliver for our shareholders."

Company Overview

Involved in the 1996 Olympic Games MasTec (NYSE:MTZ) is an infrastructure construction company that specializes in the telecommunications, energy, and utility industries.

Engineering and Design Services

Companies providing engineering and design services boast ever-evolving technical expertise. Compared to their counterparts who manufacture and sell physical products, these companies can also pivot faster to more trending areas due to their smaller physical asset bases. Green energy and water conservation, for example, are current themes driving incremental demand in this space. On the other hand, those providing engineering and design services are at the whim of construction and infrastructure project volumes, which tend to be cyclical and can be impacted heavily by economic factors such as interest rates.

Sales Growth

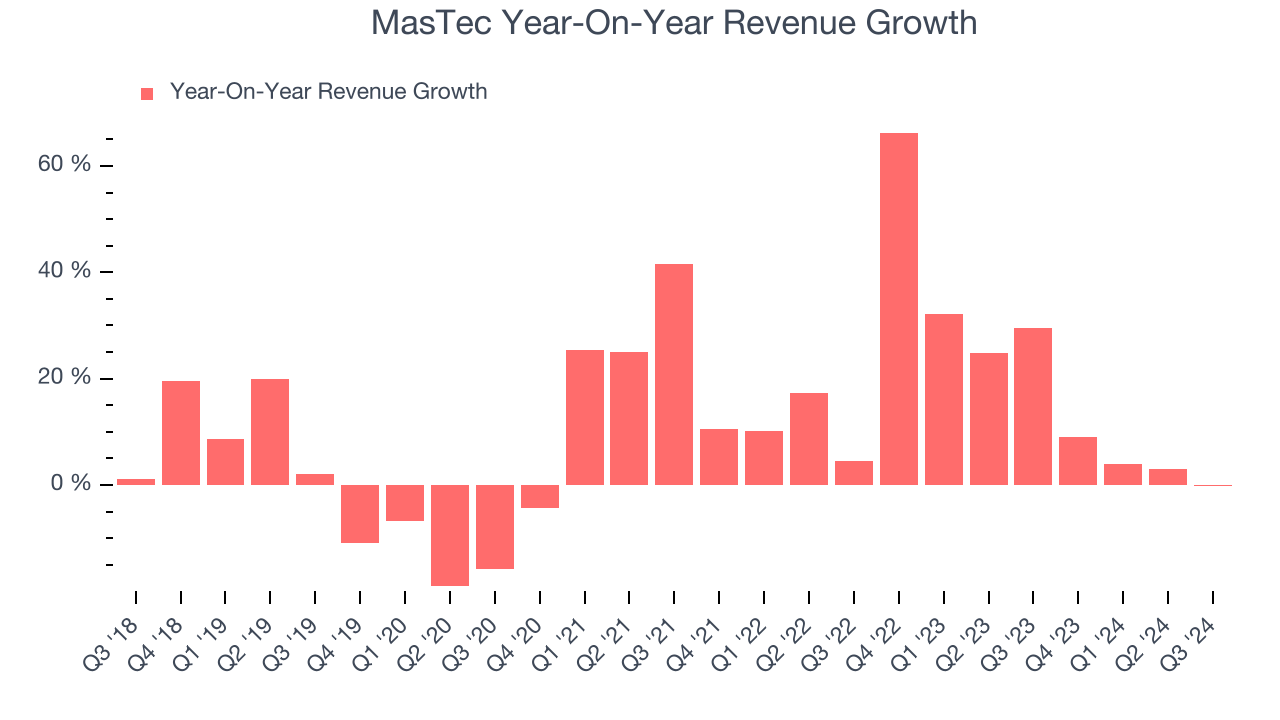

A company’s long-term performance can indicate its business quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Thankfully, MasTec’s 10.5% annualized revenue growth over the last five years was impressive. This is a useful starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. MasTec’s annualized revenue growth of 19.2% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

We can better understand the company’s revenue dynamics by analyzing its backlog, or the value of its outstanding orders that have not yet been executed or delivered. MasTec’s backlog reached $13.9 billion in the latest quarter and averaged 11.6% year-on-year growth over the last two years. Because this number is lower than its revenue growth, we can see the company fulfilled orders at a faster rate than it added new orders to the backlog. This implies MasTec was operating efficiently but raises questions about the health of its sales pipeline.

This quarter, MasTec missed Wall Street’s estimates and reported a rather uninspiring 0.1% year-on-year revenue decline, generating $3.25 billion of revenue. Management is currently guiding for a 1.4% year-on-year increase next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 9.2% over the next 12 months, a deceleration versus the last two years. Some tapering is natural given the magnitude of its revenue base, and we still think its growth trajectory is attractive.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

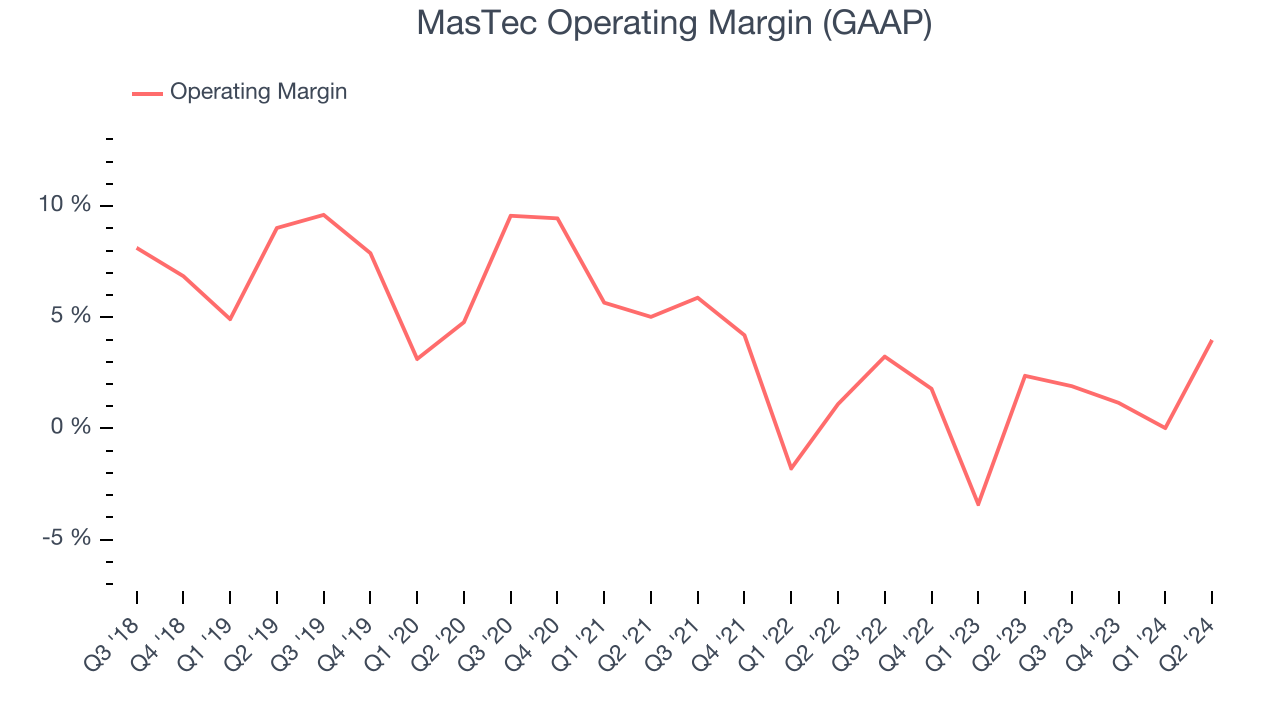

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses–everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

MasTec was profitable over the last five years but held back by its large cost base. Its average operating margin of 3% was weak for an industrials business. This result isn’t too surprising given its low gross margin as a starting point.

Looking at the trend in its profitability, MasTec’s annual operating margin decreased by 3.7 percentage points over the last five years. The company’s performance was poor no matter how you look at it. It shows operating expenses were rising and it couldn’t pass those costs onto its customers.

Earnings Per Share

Analyzing revenue trends tells us about a company’s historical growth, but the long-term change in its earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

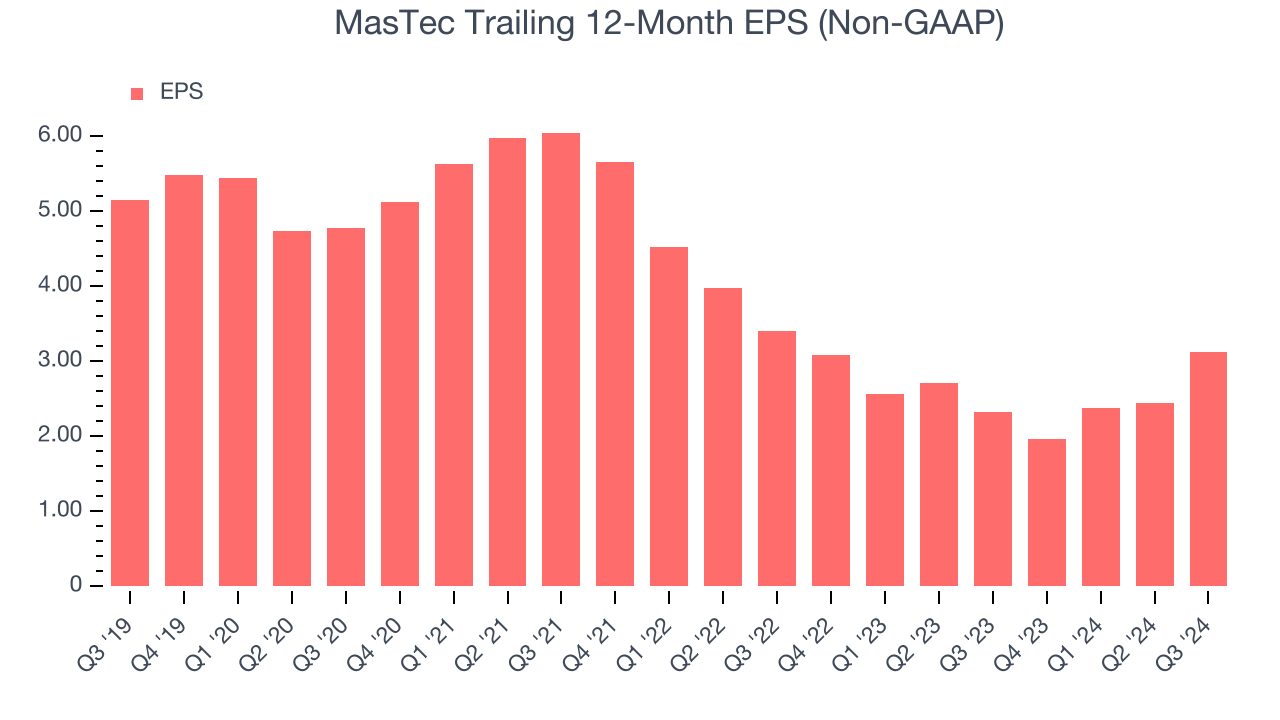

Sadly for MasTec, its EPS declined by 9.5% annually over the last five years while its revenue grew by 10.5%. This tells us the company became less profitable on a per-share basis as it expanded.

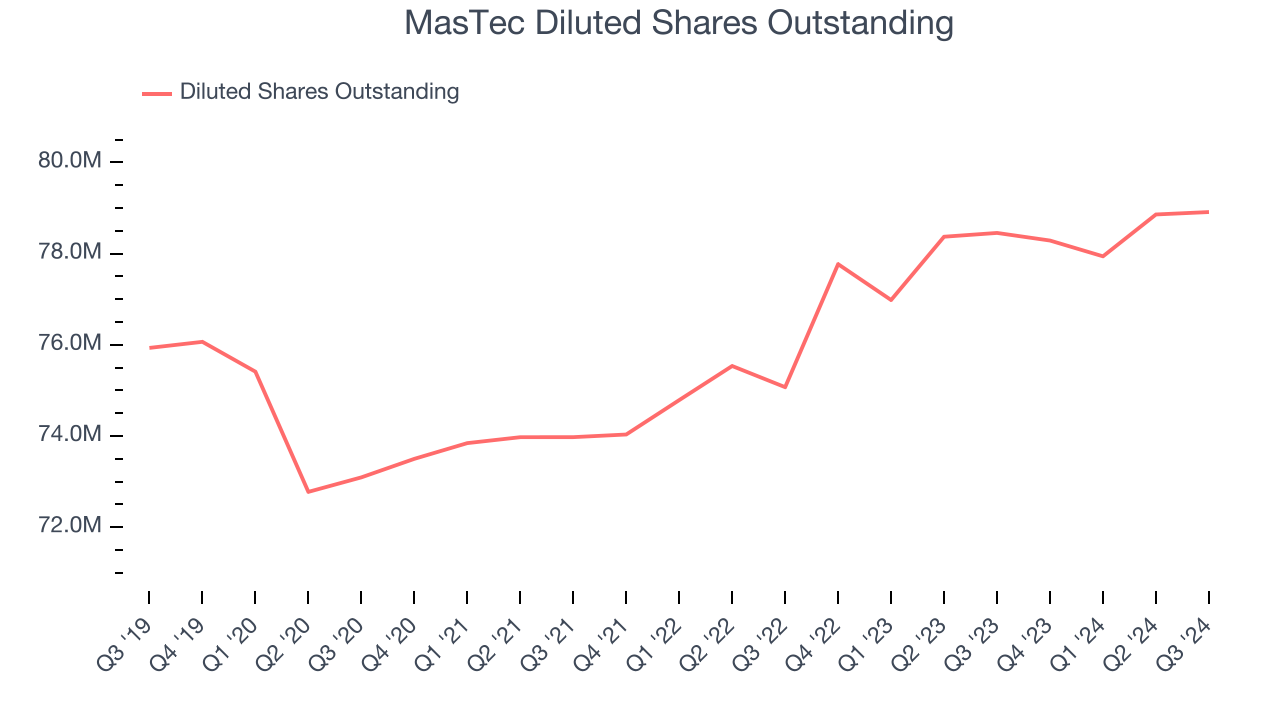

We can take a deeper look into MasTec’s earnings to better understand the drivers of its performance. As we mentioned earlier, MasTec’s operating margin declined by 3.7 percentage points over the last five years. Its share count also grew by 3.9%, meaning the company not only became less efficient with its operating expenses but also diluted its shareholders.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For MasTec, its two-year annual EPS declines of 4.2% show it’s still underperforming. These results were bad no matter how you slice the data.In Q3, MasTec reported EPS at $1.63, up from $0.95 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects MasTec’s full-year EPS of $3.13 to grow by 24%.

Key Takeaways from MasTec’s Q3 Results

We were impressed by how significantly MasTec blew past analysts’ backlog and EPS expectations this quarter. We were also excited it raised its full-year earnings guidance. On the other hand, its revenue missed, but the better-than-anticipated backlog (which shows future revenue potential) and profitability are supporting shares. The stock traded up 8.2% to $133 immediately following the results.

MasTec had an encouraging quarter, but one earnings result doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.