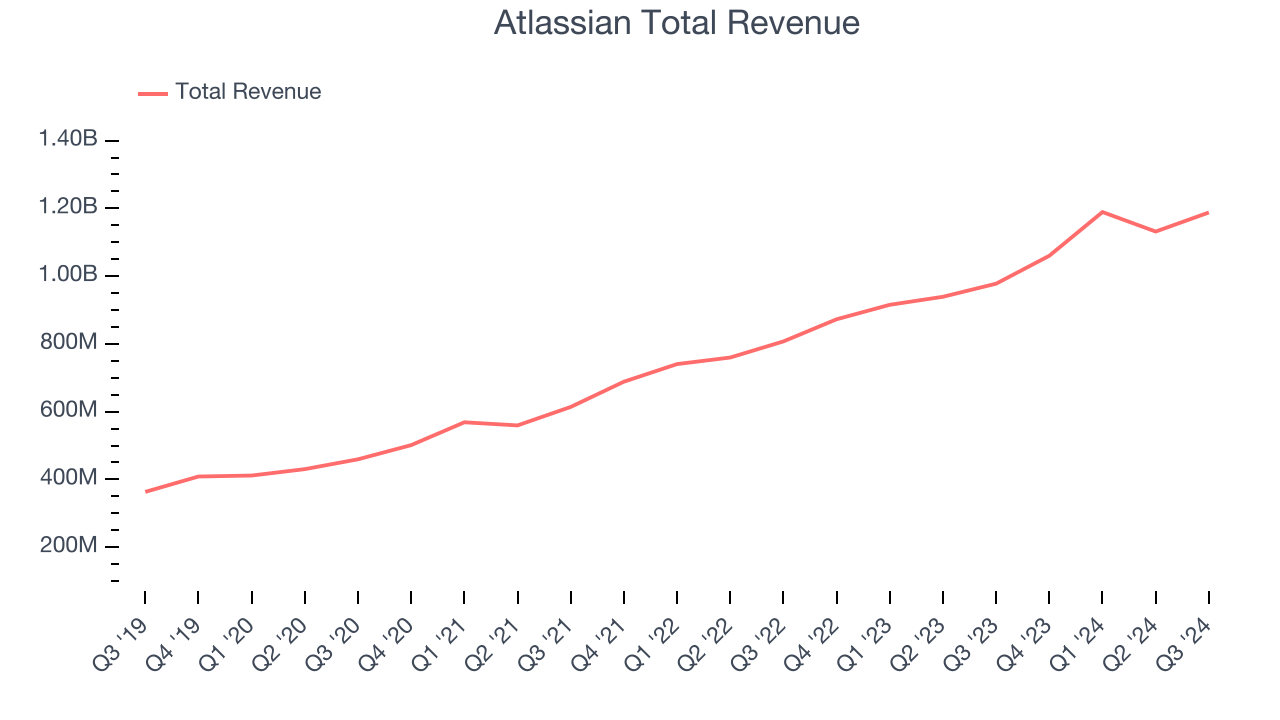

IT project management software company, Atlassian (NASDAQ:TEAM) announced better-than-expected revenue in Q3 CY2024, with sales up 21.5% year on year to $1.19 billion. The company expects next quarter’s revenue to be around $1.24 billion, close to analysts’ estimates. Its non-GAAP profit of $0.77 per share was also 19% above analysts’ consensus estimates.

Is now the time to buy Atlassian? Find out by accessing our full research report, it’s free.

Atlassian (TEAM) Q3 CY2024 Highlights:

- Revenue: $1.19 billion vs analyst estimates of $1.16 billion (2.8% beat)

- Adjusted EPS: $0.77 vs analyst estimates of $0.65 (19% beat)

- Adjusted Operating Income: $268.1 million vs analyst estimates of $220.9 million (21.4% beat)

- Revenue Guidance for Q4 CY2024 is $1.24 billion at the midpoint, roughly in line with what analysts were expecting

- Cloud Revenue Guidance for Q4 CY2024 is 27% year on year growth, above expectations

- Raised full year revenue guidance for Cloud (24% from 23%) and Data Center (20.5% from 20%)

- Gross Margin (GAAP): 81.7%, in line with the same quarter last year

- Operating Margin: -2.7%, in line with the same quarter last year

- Free Cash Flow Margin: 6.3%, down from 36.5% in the previous quarter

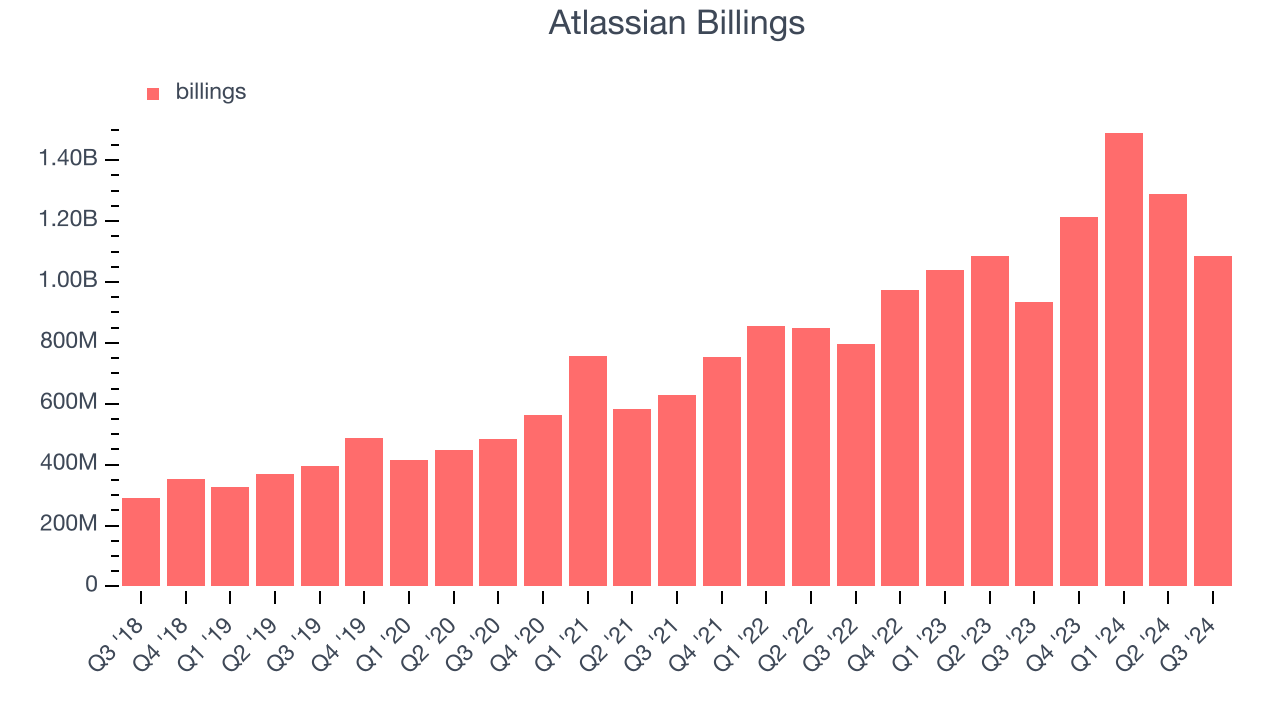

- Billings: $1.09 billion at quarter end, up 16.3% year on year

- Market Capitalization: $49.65 billion

Company Overview

Founded by Australian co-CEOs Mike Cannon-Brookes and Scott Farquhar in 2002, Atlassian (NASDAQ:TEAM) provides software as a service that makes it easier for large teams of software developers to manage projects, especially in software development.

Project Management Software

The future of work requires teams to collaborate across departments and remote offices. Project management software is both driving this change and benefiting from it. While the trend of collaborative work management has been strong for a while, the Covid pandemic has definitively accelerated the demand for tools that allow work to be done remotely.

Sales Growth

Reviewing a company’s long-term performance can reveal insights into its business quality. Any business can have short-term success, but a top-tier one sustains growth for years. Thankfully, Atlassian’s 26.7% annualized revenue growth over the last three years was solid. This is a good starting point for our analysis.

This quarter, Atlassian reported robust year-on-year revenue growth of 21.5%, and its $1.19 billion of revenue topped Wall Street estimates by 2.8%. Management is currently guiding for a 16.7% year-on-year increase next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 16% over the next 12 months, a deceleration versus the last three years. This projection is still admirable and shows the market is baking in success for its products and services.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Billings

In addition to revenue, billings is a non-GAAP metric that sheds additional light on Atlassian’s business quality. Billings is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Over the last year, Atlassian’s billings growth has been impressive, averaging 25.8% year-on-year increases and punching in at $1.09 billion in the latest quarter. This alternate topline metric has been growing faster than revenue, meaning the company collects cash upfront and then recognizes the revenue over the length of its contracts - a boost for its liquidity and future revenue prospects.

Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

Atlassian is extremely efficient at acquiring new customers, and its CAC payback period checked in at 4 months this quarter. The company’s efficiency indicates that it has a highly differentiated product offering and strong brand reputation, giving it the freedom to invest resources into new growth initiatives while maintaining optionality.

Key Takeaways from Atlassian’s Q3 Results

It was good to see Atlassian beat analysts’ revenue expectations this quarter. We were also glad its gross margin improved. Looking ahead, guidance was strong, with next quarter's cloud revenue growth of 27% year on year strong and above expectations. The company also raised its full year revenue guidance for Cloud and Data Center. There had been doubts about topline momentum, especially for Cloud revenue, so this quarter puts a big dent in the bear case. Overall, this was a very solid quarter. The stock traded up 15.7% to $218 immediately following the results.

Should you buy the stock or not? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.