The spring season is finally upon us! Time to pull out the raincoat, plant some seeds and put that green thumb to use.

If you’re a stock trader, it’s also a time to put on the thinking cap. First quarter earnings season is upon us — which means plenty of opportunities for new portfolio growth. And on the heels of a volatile market for March 2023, traders could be in for a wild ride.

Due to recession and bank liquidity concerns, Wall Street analysts have set the bar low. Data from FactSet shows that S&P 500 companies are expected to report 6.6% lower earnings for the first quarter of this year. If they do, it would be the group’s biggest earnings decline since the coronavirus outbreak.

While this suggests storm clouds are rolling in, there’s actually a ray of light. With low-profit expectations come opportunities for sizable outperformance.

If early reports are any indication, there will be plenty of positive surprises ahead. Of 17 S&P companies that reported first-quarter results through March 31st, all but one beat consensus earnings per share (EPS) estimates.

Where will future beats come from?

Quite possibly from sectors that are expected to have witnessed growth. According to Factset, industrials, financials and consumer discretionary names are expected to have survived demand slowdowns and cost inflation better than most. This makes these three stocks bullish swing trade candidates.

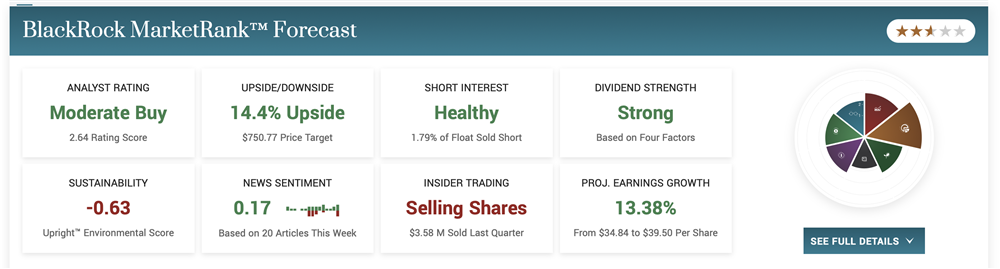

What Could Drive a Black Rock Earnings Beat?

Since the capital markets have trended lower since late 2021, BlackRock, Inc. (NYSE: BLK) faces tough year-over-year comparisons. As such, analysts have set the Q1 bar low — but as we learned from recent results, it may be too low. BlackRock has topped quarterly EPS expectations by a wide margin the last two times out. Higher interest rates attracted investors to the company’s fixed income products in Q4, driving a 10% positive earnings surprise.

With interest rates only increasing since it could be déjà vu when BlackRock reports first-quarter results on April 14th. Considering recent layoffs, strong bond inflows and lower costs could drive another meaningful EPS beat.

In worst case scenario, if a bullish earnings trade fails, the position could be converted into a longer-term holding. At 20x earnings, BlackRock is trading slightly below the capital market industry average when its growth profile arguably supports a premium valuation.

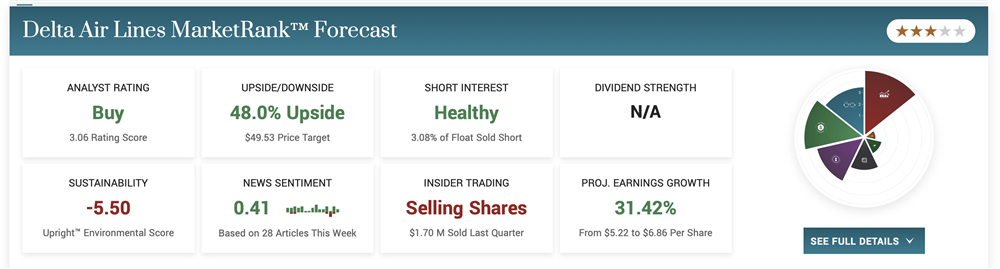

Is Wall Street Bullish on Delta Air Lines Stock?

Delta Air Lines Inc. (NYSE: DAL) kicks off airlines earnings season on April 13th. Being the lead-off batter makes it harder to glean information from peer reports, but the stock may be worth a swing. Led by strong travel demand, Delta beat last quarter’s earnings bogey by 5%. Developments since have been mixed.

Travel restrictions in Western Europe and China have been lifted, boosting international travel. Business travel is also on the rebound with corporate events and conferences back in full swing. On the negative side, kerosene jet fuel prices have soared to a multiyear high and labor costs are up. This sets the stage for an intriguing tug-of-war between increasing revenue and increasing costs.

Last time around, demand won out, propelling Delta to a double beat. However, management’s 2023 earnings guidance reflected high costs associated with labor deals and an operations ramp ahead of the summer travel season. The stock sold off, but the airliner’s outlook may prove overly cloudy.

Higher-priced corporate and international tickets can potentially drive strong top-line results over the next few quarters. This is a big reason why the Street is unanimously bullish on Delta. Three analysts have upgraded to buy this year — and with price targets in the $ 40s and $ 50s, the first quarter update could ignite a powerful takeoff.

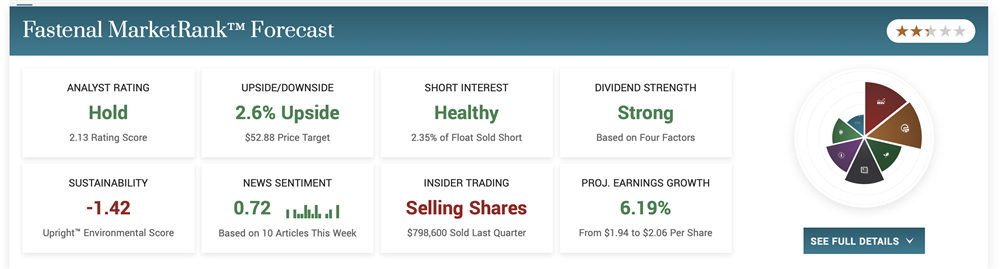

What Could Cause Fastenal’s Share Price to Go Up?

When Fastenal Co. (NASDAQ: FAST) reports first-quarter numbers on April 13th, the market will look for 6% EPS growth. This would be the lowest year-over-year growth in nearly two years.

But after beating both Q3 and Q4 EPS estimates, the industrial supplier kicked off 2023 by announcing a 13% dividend increase. This signals confidence in the long-term outlook, which could manifest as early as next week’s Q1 report.

Granted, Fastenal still has some challenges to hammer out. Construction activity has slowed, and operating costs have increased. At some point, Fed rate hikes will stop, which would boost mortgage activity and Fastental’s business. This certainly won’t be reflected in first-quarter results, but upbeat management commentary about an expected housing market recovery could push the stock higher regardless of the Q1 performance.